WARNING: Is a Banking System Collapse Imminent?

Wed 9:37 am +01:00, 5 Oct 2022 1

by Brian Shilhavy

Editor, Health Impact News

As I write this on Tuesday, October 4th, 2022, the stock market in the United States is up significantly, for the second day in a row.

And yet even in the Corporate Media financial publications, which tend to emphasize the positive for investors, the news about what the immediate future holds is very gloomy today.

Here is one example from MarketWatch today which I saw on their homepage at the same time that the DOW was up almost +800 points, which featured an interview with Keith McCullough, founder and CEO of Hedgeye Risk Management.

“An entire generation of Americans hasn’t gone through a recession. A lot of companies in Silicon Valley have never been through a recession, for example. My definition of a U.S. corporate profits recession is when the rate of change of revenue growth has gone negative and the rate of change of year-over-year profit growth has gone negative. The Federal Reserve, even if it were to turn dovish on interest rates tomorrow, will have a hard time stopping the profits recession.

When the rate of economic change is accelerating and the Fed is printing money, you buy anything that’s got a good chart and a good story. You’re going to make a lot of money until the music stops.

And it did. Now we’re seeing the opposite. The rate of change of real GDP growth and inflation are slowing at the same time. You can’t own inflation, commodities or growth now. If you’re still long pretend growth or profitless growth or crypto, I recommend prayer.” (Source.)

When a corporate financial news source features an interview on their homepage from a financial investment CEO who says “I recommend prayer,” it is time to sit up and pay attention to what may be about to happen.

And while this CEO does not discuss possible bank failures, there are plenty of others today who are, based mainly on two international mega banks that seem to be on the brink of collapse: The Bank of England, and Credit Suisse.

What does a potential collapse of the banking system mean for you? Here is one analyst’s view:

“During banking crises, you won’t have full access to your deposits in the bank. As a result, electronic payments such as bank cards may become useless. In the extreme case, your deposits could be used to recapitalize ailing banks in a process called ‘bail-in.’”

Here are some examples of financial news reports that are being published today warning about bank failures that you may not read in the Corporate News.

A Banking Crisis Looms

by Tuomas Malinen of The Epoch Times via ZeroHedge News

My columns have turned rather apocalyptic of late, but for a valid reason. Just this week, we got confirmation that our financial system is, again, on the brink of collapse, when the Bank of England (BOE) was forced to enact, de facto, a bailout of the pension funds of the United Kingdom.

On Sept. 28, around noon, the Bank of England stepped (back) into the gilt markets and started buying government bonds with longer maturities to stop the collapse in their value, which could have caused the financial system to become unhinged. Pension funds were faced with major margin calls, which threatened to cause a rapidly cascading run on their liabilities, as trust in their liquidity and solvency would have become questioned by a widening circle of investors and customers.

Effectively, the BOE stepped in to limit the vicious circle of margin calls faced by pension funds because of the crashing values of the gilts.

Without the BOE intervention, mass insolvencies of pension funds, with about $3 trillion worth of assets—and thus most likely other financial institutions—could have commenced on that afternoon. It’s obvious that if one of the major financial hubs of the world, the City of London, would face a financial panic, it would spread to the rest of the world in an instant.

It looks as though the global financial system was pulled from the brink of collapse, once again, by central bankers. However, this was only a temporary fix.

It’s now clear that an outright financial collapse threatens all Western economies, because if pension funds, often considered very dull investors because of their risk-averse investing profile, face a threat to their insolvency, it can happen to any other financial institution. I consider that the banking sector will be the next in line.

Banking is a business of trust. If the trust in a bank or in the unlimited support of authorities for the bank, disappears, a bank run commences.

One of the most prominent scholars of financial crises, Gary B. Gorton, defines a financial crisis in his book “Misunderstanding Financial Crises: Why We Don’t See Them Coming” as “an event where holders of short-term debt issued by financial intermediaries withdraw en masse or refuse to renew their loans.”

In common language, Gorton says that during financial crises, a large number of holders of banks’ financial liabilities, such as deposits, want to cash out. Hence the name: a bank run.

For example, during the Panic of 1819 in the United States, people queued outside banks in long lines to change their new financial innovations, bank notes, to metallic currency. The Panic of 1819 helped to create the first economic depression in the United States.

However, a bank run may not be visible, in the sense that other banks and financial institutions “run” on the liabilities of a bank. For example, during the crisis of 2007–2008, there was a run on sale and repurchase agreements (repo) market, market of commercial paper, and on prime broker balances. Most people didn’t notice these first stages of the panic, because financial firms ran on liabilities and assets of other financial firms.

The main point is that, as liabilities are withdrawn in whatever form, en masse, the bank eventually runs out of assets to pledge/sell to fulfill the withdrawal requests, and the bank fails.

Going forward, the biggest risk of a systemic bank run most likely lays in Europe.

European companies and households have been and continue to be decimated by ravaging inflation, fast-rising interest rates, and spiking energy prices. They are being hit on all sides, and this will, most likely, cause many of them to fail financially.

Banks are also currently being hit by heavy declines in the value of government bonds, which they use as collateral. These may easily lead to cascading losses on banks, possibly with a never-before-seen speed, size, and width.

I find it hard to imagine how these developments wouldn’t lead to a banking crisis, without massive intervention by governments and central banks, that is. And like I’ve been detailing, a banking crisis that begins in Europe, won’t stay there.

How do you prepare for it then?

A characteristic feature of a banking crisis is that many banks, possibly all, will close their doors to customers, and issue withdrawal limits. Another characteristic is disruptions in the financial system, most notably on card payments, as a result of which the retail payments system may seize up altogether.

While I was in Greece, in the summer of 2015 with my ex-wife, the whole economy turned into a cash-based one basically over the weekend. The 2015 Greek banking crisis was caused by the European Central Bank, when it, totally irresponsibly and most likely driven by political motives, shut Greek banks from its emergency liquidity assistance.

Cash withdrawal limits were set, credit card machines “disappeared” or “broke down” in restaurants, shops, and more, and finally, cash stopped coming out from the ATMs. Capital controls were enacted, and the ability of ordinary Greeks to transfer money abroad became seriously hindered. We naturally had sufficient cash, which often happens, when one travels with a crisis researcher to a country threatened by a crisis.

The main point is (was), that during banking crises, you won’t have full access to your deposits in the bank. As a result, electronic payments such as bank cards may become useless. In the extreme case, your deposits could be used to recapitalize ailing banks in a process called “bail-in.”

Such laws were put in place after the 2008 crisis, and they were enacted for the first time to resolve the banking crisis in Cyprus in 2013.

Technically, every sum you have in the bank above the deposit insurance threshold, a limit which also may not be “carved in stone,” is threatened by the bail-ins in a banking crisis.

We warned already in March 2017 that the global financial system, which broke out during the 2008 financial crisis, has never really been healed. We noted that it and the global economy were kept standing merely by continuous central bank and government interventions and nearly unlimited provisions of credit. On Sept. 28, we got a final confirmation from the BOE that this truly is the case.

We are in deep, deep trouble.

Read the full article at ZeroHedge News.

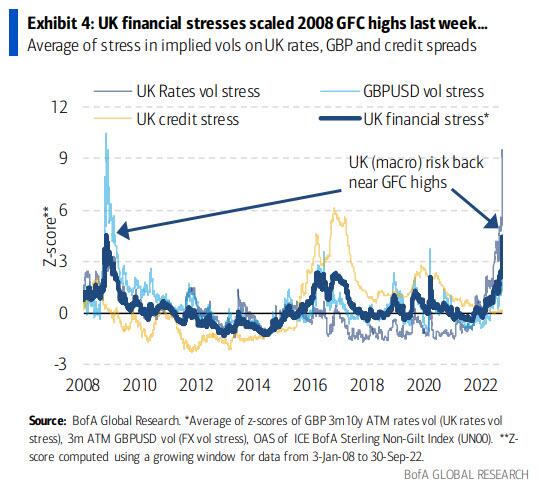

BofA Warns Of ‘Bear Stearns Moment’ If Central Bank Put Fails

Last week’s UK crisis was a reminder of how dependent markets are on central bank support, and the dilemma they face in maintaining market stability in the face of furious inflation.

As BofA writes in a note this morning, not since Greenspan invented the central bank put in the ’87 crash have they been this constrained and we see the biggest visible tail-risk as a test & fail of the Fed put.

Crucially the bank points out that the UK events also highlight that even when a risk is well-telegraphed (global tightening), markets remain full of hidden risks.

Specifically, BofA draws five lessons from last week’s UK crisis, as it corroborated several concerns and made clear the risks emerging from today’s policy and market environment:

1. Painful withdrawal: A highly-levered system “addicted to doves” is being rudely awakened by the fastest, most aggressive monetary policy tightening in over 40yrs, and wide cracks are emerging.

2. Hidden risks: Even when the main risk facing markets is visible and relatively slow-moving (as CB tightening has been this year), markets are full of hidden risks and non-linearities that only reveal themselves in times of stress. We’ve been partly attributing the complacency in equity vol this year to the well-telegraphed nature of the catalyst. But this episode should remind equity investors of the existence of “unknown unknown” secondary effects (at times coming from abroad) and force them to price in a thicker left tail in stocks. We have indeed seen a notable jump in some equity vol risk premia following last week’s events, primarily in Europe but also in the US to a lesser degree.

3. Testing the Central Bank put: The trade-off between fighting inflation and maintaining financial stability is a complication for central banks not faced in 35 years since the central bank put was invented. The BoE had to pause their inflation fight last week to restore financial stability, and the Fed could be close to having to do the same, as we argued previously (plus, our rates strategists say risks of a breakdown of Treasury market functioning are growing).

4. Relief only temporary: The BoE’s intervention prevented a real catastrophe for UK assets. But the emergency policy response didn’t fix the underlying problem, namely the highest rates of inflation in decades. In fact, the BoE’s actions in the Gilt market are counter to their stated inflation-fighting plan, and each test of the central bank put may see less and less of a calming impact on markets. If the BoE put were to fail (or the next test of a central bank put), the risk is that it’s akin to the Bear Stearns moment of the 2008 crisis, causing investors to further question central banks’ ability to provide protection in the era of high inflation. The Fed facing a similar dilemma and failing would be the Lehman moment.

5. Dented Central Bank credibility: In fact, even the relief rally after the BoE intervention was underwhelming compared to other central bank rescues post-GFC. The S&P 500 hit new YTD lows several times in that same week, as did the local FTSE 100. To us, this is a sign that central bank credibility is already dented, and strengthens our view that the biggest risk to markets is a test & fail of the Fed put.

Reflecting on these lessons, BofA warns that historic moves in Gilts and Sterling akin to those seen last week have the ability to cause further contagion and add further pressure on central banks that are already constrained by persistent inflation. The path to contagion, though not the base case, can be rapid. Indeed, the recent re-pricing of derivatives convexity serves as a reminder that tail risks aren’t dead and the bank continues to recommend investors concerned about risk combine hedges for a grind lower with more convex protection.

The next test of the CB put (in the UK or elsewhere) may not be so easy to remedy without the ability to do “whatever it takes” for as long as it takes.

And if the BoE put were to still fail (they are not out of the woods yet), the risk is that it’s akin to the Bear Stearns moment of the 2008 crisis. The Fed facing a similar crisis would be the Lehman moment in our view.

Timing this risk is hard and oversold markets could create another June like bear-rally. Between Bear and Lehman, the S&P rallied 10% before selling off.

But any risk-rally is also a good time to enter hedges, and we continue to suggest smart grind-lower coupled with cheap to carry convexity hedges.

Interestingly, BofA sees ‘Gold Calls’ as ranking cheapest versus their potential realized tail risks.

Additionally, BofA sees IEF calls, LQD puts and HYG puts as screening best as hedges, offering the highest proportion of extreme gains vs current costs.

As BofA notes, its far from all-clear with respect to UK risk, and if last week was any guide, we are watchful of further contagion to financial assets outside the UK.

Read the full article at ZeroHedge News.

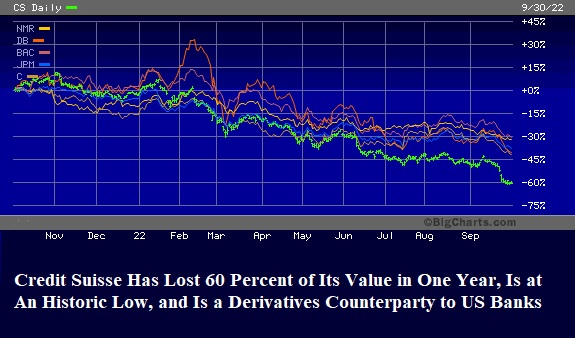

Here’s the Chart of the Global Bank Causing Panic in Markets This Morning

by Pam and Russ Martens

Wall Street on Parade

The Swiss global bank, Credit Suisse, which is a derivatives counterparty to major Wall Street banks and U.S. insurers, raised alarm bells in markets on Friday and is raising more anxiety this morning. Its 5-year credit default swap (CDS), a measurement of its risk of defaulting on its debt, jumped to 250 basis points on Friday and traded as high as 350 basis points in early morning trade today.

The big move in the CDS on Credit Suisse is further impacting the price of its common stock. The shares closed on Friday in New York at $3.92, just pennies away from its all-time low, then dropped another 11 percent in early morning trading in Europe today.

When a major derivatives counterparty begins to see a blowout in its credit default swaps, that impacts the stock prices of all major Wall Street banks with significant exposure to derivatives. It also raises the risk of systemic contagion — as occurred in the financial crisis of 2008 when Citigroup and Lehman Brothers were teetering and were major derivative counterparties. The chart above shows the dramatic declines in not just Credit Suisse over the past year but in Nomura (NMR), Deutsche Bank (DB), Bank of America (BAC), JPMorgan Chase (JPM), and Citigroup (C).

The reputation of Credit Suisse has taken major hits in the past few years. On March 26, 2021, the family office hedge fund, Archegos Capital Management, defaulted on margin calls to its prime brokers and went belly up, leaving major investment banks with more than $10 billion in losses. Credit Suisse took the lion’s share of those losses, acknowledging a loss of more than $5 billion.

To understand the nature of the wildly risky structure of the derivatives that led to the blowup of Archegos, see our report: Archegos: Wall Street Was Effectively Giving 85 Percent Margin Loans on Concentrated Stock Positions – Thwarting the Fed’s Reg T and Its Own Margin Rules.

Credit Suisse was also deeply enmeshed in the Greensill Capital scandal and has suffered serious reputational damage as a result.

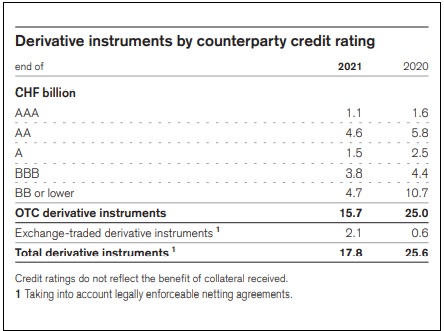

Making stock investors equally nervous is the fact that Credit Suisse admitted in its 2021 Annual Report that some of its billions in derivatives are difficult to accurately price. It writes:

“In addition, the Group holds financial instruments for which no prices are available and for which have few or no observable inputs (level 3). For these instruments, the determination of fair value requires subjective assessment and judgment depending on liquidity, pricing assumptions, the current economic and competitive environment and the risks affecting the specific instrument. In such circumstances, valuation is determined based on management’s own judgments about the assumptions that market participants would use in pricing the asset or liability (including assumptions about risk). These instruments include certain OTC derivatives, including interest rate, foreign exchange, equity and credit derivatives, certain corporate equity-linked securities, mortgage-related securities, private equity investments, certain loans and credit products, including leveraged finance, certain syndicated loans and certain high yield bonds.”

Under “Major Risks,” the 2021 Annual Report for Credit Suisse calls out the following risk for its Investment Bank:

“Loan underwriting and lending commitments to corporate clients, markets and trading activities including securities financing and derivatives products with global institutional clients, including banks, insurance companies, asset managers and hedge funds; through the use of derivatives clients may take positions that are exposed to movements in risk factors such as interest rates, credit spreads, foreign exchange rates or equity prices.”

All eyes on Wall Street are going to be watching the price action of Credit Suisse and other major banks on Wall Street this week in an effort to discern which banks are most heavily exposed to Credit Suisse as a derivatives counterparty.

Derivatives by Counterparty Credit Rating Reported by Credit Suisse in Its 2021 Annual Report

Credit Suisse and the Fed’s Plunge Protection Team

by Pam and Russ Martens

Wall Street on Parade

At 6:53 a.m. this morning (ET), Dow futures were up 454 points. That followed the Dow Jones Industrial Average gaining 765 points yesterday. No one who has been a trader on Wall Street or a stock broker for multiple decades believes this rally is real. Wall Street veterans are thinking that either the Fed’s plunge protection team or the Treasury’s plunge protection team is behind the rally. Equally unbelievable, as the chart above indicates, is the fact that the major mega banks on Wall Street closed in the green yesterday. Many of these are counterparties to Credit Suisse derivatives and thus subject to the potential for contagion.

Until everyone who works on Wall Street is 25 years old and too young to remember what happened in 2008 after Citigroup began to quake, Wall Street traders are not going to believe that the Dow can stage a legitimate rally or even a short squeeze rally when a Global Systemically Important Bank (GSIB) such as Credit Suisse is blowing out its Credit Default Swaps (CDS).

The 5-year CDS of Credit Suisse has spiked from a reading of 55 basis points in January to an historic intraday high of more than 350 basis points on Monday. The price of a Credit Default Swap reflects the cost of insuring oneself against a debt default by the bank. Who would be stampeding into the CDS of Credit Suisse and driving up the cost of protection? The mega banks on Wall Street that are counterparties to its derivative trades come to mind, as well as hedge fund speculators.

Credit Suisse is Switzerland’s second largest bank, after UBS. It is also a major trading house on Wall Street and a derivatives counterparty to other global banks. Its shares tumbled to an intraday historic low on Monday before closing up in New York, but still at the single-digit price of $4.01. The shares of Credit Suisse have lost 58 percent of their value year-to-date, based on yesterday’s closing price – far worse than its peer global banks.

Various analysts on Wall Street were issuing votes of confidence on the bank yesterday. Unfortunately, one can’t rely on the analysts at other global banks on Wall Street to tell the truth about how bad the situation is at Credit Suisse. The derivative desks of these same banks are highly likely derivative counterparties to Credit Suisse and could lose billions of dollars if it defaults and catch the contagion it leaves in its wake. In fact, many of these banks are likely demanding more cash collateral from Credit Suisse on those derivative trades as we type these words.

The panic around Credit Suisse has been growing as its share price dived this year and last after the bank suffered over $5 billion in losses from its tricked-up derivatives with the family office hedge fund, Archegos Capital Management. Archegos went belly up in March of last year. Credit Suisse’s reputation took another hit from its involvement in the Greensill Capital scandal. Then, of course, there was the infamous spy-gate scandal in 2019 where the bank spied on and followed various employees. (You can’t make this stuff up.)

The panic moves around Credit Suisse’s shares and CDS on Monday were fueled by a Tweet that went viral on Saturday. ABC business reporter, David Taylor, Tweeted this statement: “Credible source tells me a major international investment bank is on the brink.” The Tweet was subsequently removed after it had been retweeted more than 4,000 times.

Dennis Kelleher, President of the nonprofit watchdog, Better Markets, released the following statement yesterday on the situation:

“As the financial condition of Credit Suisse continues to deteriorate, raising questions of whether it will collapse, the world and U.S. taxpayers should be deeply worried as multiple, simultaneous shocks shake the foundations of economies worldwide. Credit Suisse is a global, systemically significant, too-big-to-fail bank that operates in the U.S. and is deeply interconnected throughout the global financial system. Its failure would have widespread and largely unknown repercussions from the inconvenient to the possibly catastrophic.

“That is due, in part, to the failure of the Federal Reserve to properly regulate the activities of foreign banks that have U.S.-based operations. The U.S. has a largely ineffective regulatory framework with gaping loopholes that fail to include some of even the most basic safety and soundness requirements, which incentivizes regulatory arbitrage. As a result, the U.S. financial system and economy are needlessly threatened.

“An effective and appropriate regulatory framework for large foreign banks that covers all of their U.S.-based affiliates should have been established when the Fed set up so-called U.S.-based intermediate holding companies (‘IHCs’) that they regulate. Instead, U.S.-based branches of foreign banks (which are not consolidated within the IHC) face significantly weaker standards than the IHC, remarkably including no specific capital requirements in the U.S. Furthermore, the branches have significantly weaker liquidity requirements. This has resulted in many foreign banks – including in particular Credit Suisse – engaging in regulatory arbitrage by shifting large amounts of assets from their IHCs to their branches, entities that are entirely reliant on the resources of their foreign-based parent companies. The 2008 financial collapse proved that these resources are not available in periods of stress, which is why the U.S. bailed out so many foreign banks operating in the U.S. The Fed should have stopped that long ago.

“As is well-known, risks in the global financial system that materialize elsewhere easily end up becoming risks here in the U.S. and threaten our financial system and economy. Those risks are amplified by the unprecedented fiscal and monetary policies attempting to address the many unexpected shocks from the pandemic and war. The Fed must see Credit Suisse as a warning sign and improve the regulatory framework for large foreign banks and all banks to ensure that the American financial system and economy are properly protected.”

Lisa Gilbert, Executive Vice President of another nonprofit watchdog, Public Citizen, released this statement:

“The tumult at Credit Suisse was brought on by the bank’s own penchant for recklessness and risk-taking, which caused market participants to lose confidence in its ability to withstand changing conditions, such as this year’s rise in interest rates and significant commodity volatility – highlighting that financial regulation remains extremely relevant and important. Regulators must remain vigilant – given the risks giant financial firms pose to the global financial system – and work to complete the long overdue rule from the Dodd-Frank Wall Street Reform Act that would deal with risky CEO behavior incentivized by huge pay packages.”

Read the full article at Wall Street on Parade.

The Chinese will still buy the dollar. By the ton, to fuel their power stations.