Lockdowns Push Greece Towards Another Financial Crisis [VIDEO]

Fri 4:02 pm +01:00, 18 Dec 2020

- The Greek economy is unfit for purpose: overtaxed and over regulated. Greek state is a major burden on the economy – it is parasitic upon it and far too large. Austerity imposed on Greece after 2008 crisis has EXACERBATED all those problems. It punished the productive parts of the economy such as they were; they were weighed down by taxes and pushed out. It’s much easier to work for the govt than it is to set up your own business. The size of the state, the patronage system (a major blight on Greece), and its regulatory system were all intensified! The crisis caused more people to look to the state to fix the problem, yet the state just exacerbated it.

- The Greek system of corruption, a fundamental obstacle to reform, was made all the worse. European money received post-crisis was used to sustain this model. The Greek economy was made even more unproductive and uncompetitive, which made it more dependent on state handouts. So what the EU did was to make the underlying problems worse. It was all predictable. But EU officials and political / oligarchic Greek classes were just fine with it. They ended up stronger for it. It was done by design.

- As things get worse, more and more state property will have to be sold off. The new Greek government has failed to fix economic problems and liberalize the economy. The pandemic has just made things worse. Debt-to-GDP ratio is at 200%. Greek economy shrunk by 14% in Q2 of 2020. Govt. budget deficits have risen. ‘This could be coming to a European country near you.’

- 50% of the population is dependent on the public sector. It’s a red flag for every country. Its public sector is completely parasitic: it doesn’t have Volkswagen, for example, which is part government owned in Germany. Govt is the major provider of jobs and income; this group votes for the political class in power at any given time. The system never changes in Greece.The underlying macro-economic problem needs addressing, which is that the Govt is not accountable to the people. It gets propped up by the EU in Brussels and Berlin. It is saddled by an uncompetitive exchange rate which discourages outside investment in the economy. Greece cannot devalue its currency to make it competitive because it has the euro and has no power to do that. In the ’50s and later, Greece was beginning to develop its own manufacturing sector, but this was crushed after joining the EU. The Greek political and oligarchic class in Greece is just fine with the way things are – these state-appointed officials, civil servants and business owners are just bound together in a corrupt, state-controlled system. Any income made from business is just recycled and never has any productive use; it is just used for corrupt purposes.

- Greece doesn’t produce anything anymore and sold off its biggest port under Tsipras years ago. The govt is likely to sell off more state assets and the people won’t know until disaster happens. This is typical of Greece.

- The first lockdown dragged on longer than announced; the tourist industry was expected to turn things around. But it did not come in and save the economy. Now they’re in a 2nd lockdown, which has been extended and will crush the economy. Society is so split because half of it has no problem, the part employed in the public sector; but the privately-employed half is getting pummelled. So the productive side of the economy is being run-down. So the state is left, and it grows, which strengthens the corrupt state of the country. Greece will be the extreme example of this tendency within Europe, which is being locked down with similar economic effect. Greece will be the indicator of how bad things are.

- The whole point way back after the 2008 crisis was to bring Greek debt levels DOWN, ostensibly. But it was indebted far more, and now we see it exploding. It’s trapped inside the eurozone, so that much of its debt has been transferred over time from debt owned by banks (private) to the taxpayer (public). Greece can’t get its debt problems with private banks fixed because it would have to have taxpayers in other European countries approve THEIR PAYING OFF of Greece’s debt at their own expense. Merkel took Greece’s situation and made it worse: the system that created the problem became entrenched and more powerful. The resulting economic/political system means there are no democratic ways to fix the problem. Greece will have to crash completely in order for the system to begin again.

- The govt should never have done a second lockdown. There were other ways to deal with it, including a sunny climate and vitamins. PM Mitsotakis has killed the country. The first lockdown was not done in response to the actual infectious situation at the time – it was done to impress the paymasters in Berlin, Frankfurt and Brussels. The second one is crushing it. The Greek economy has been in crisis for 10 years, and now it can’t be ended. The debt-to-GDP ratio has GONE UP over this time instead of going down as intended. It Greece had been a sovereign country with commercial debt problems, it would have agreed a restructuring with its creditors, which can work. It would have provided a path forward. But instead, it was forbidden to restructure: it was forced to convert its commercial debt into debt OWED TO EU INSTITUTIONS, which is still there and cannot be ended in any way. The country is left trying constantly to maintain this debt, and accept austerity conditions on top, which destroy its productive economy. And the euro makes it uncompetitive, deterring investment. There are many Greeks living outside of it, but are not encouraged to invest in it. The red tape and corruption in the country make the problems worse. Only the Greek political class, the bureaucracy in the EU and Greek oligarchs benefit from it.

- Greece is the canary in the coalmine because other EU countries are going the same way, such as Italy, which has a major manufacturing base that is contracting with each year. Italy is very entrepreneurial but it cannot become productive, either. It has similar problems to Greece. Italy is now where Greece was 30 years ago. The decline in Italy and Spain is progressing quickly. Locked into the EU, they can’t regain their economic dynamism and work productively.

**********

Lockdowns push Greece towards another financial crisis

****

Greece Is Setting Itself Up for Another Financial Crisis

ANTONIS GIANNAKOPOULOS

Listen to the Audio Mises Wire version of this article.

The Greek economy shrunk by a record 14 percent in the second quarter of 2020 while at the same time government efforts to ‘’cure’’ the economy have set the country on the road to cross the 200 percent debt-to-GDP ratio as the IMF forecasts. In the meantime, government budget deficits have reached new heights (around 7 percent).

The Government’s Response to the Recession

The Greek government tried to combat the economic downturn with a loose fiscal and monetary policy (through the European Central Bank). The initial aim was to support pretty much everyone from the public and private sector for the bad months of the covid-19 lockdown and hope for economic recovery when the summer arrived, with the tourist industry saving the day. It soon became evident, however, that this was wishful thinking. People from the tourist industry admitted that it could take years for the industry to recover its past numbers. The situation looked even worse once people realized how dependent the whole economy is on tourism: it accounts for 20 percent of GDP and provides 22 percent of all employment in Greece. Furthermore, the Greek government’s solutions, like those of most of the other governments in Europe, were primarily demand-side policies.

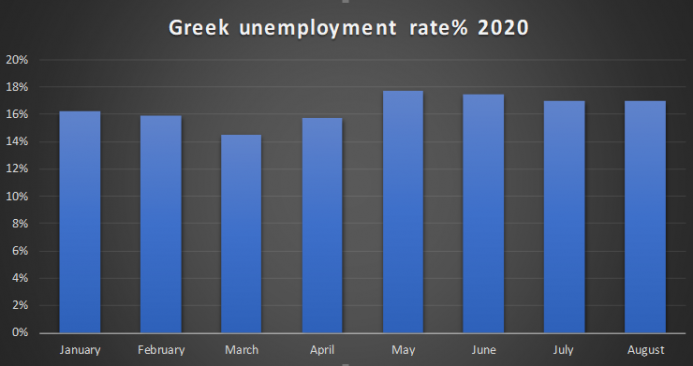

As I predicted in one of my past articles, these measures could only provide short-run relief, only postponing the pain until later. The unemployment rate saw a 1.2 percent increase from March to April, of 1.3 percent from April to May, and it saw a minor decrease during the summer tourist period. The Organisation for Economic Co-operation and Development (OECD) has estimated that the unemployment rate will reach roughly 20 percent by the end of the year.

Source: Trading Economics.

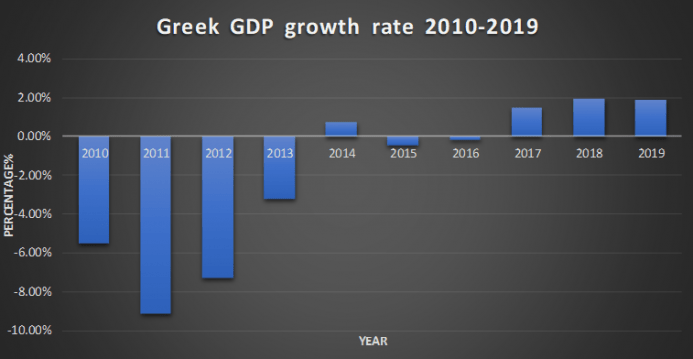

In the meantime, that the GDP saw a 14 percent contraction in the second quarter means that the Greek economy will need years to reach its pre-corona numbers, especially considering its anemic growth rate over the last decade.

Source: International Monetary Fund, World Economic Outlook: The Great Lockdown (Washington, DC: International Monetary Fund, April 2020).

What Went Wrong?

The ECB’s balance sheet had a massive increase from 39 percent of the GDP to 54 percent during the summer. In comparison the Fed’s balance sheet is around 32 percent of GDP. The injections of liquidity via the ECB have effectively zombified a considerable number of companies in the EU, with corporate debts reaching new highs. In the case of Greece, the government has exploited its new, EU-sanctioned fiscal leeway, which has allowed it to perpetuate structural problems in its economy along with large deficits. During the tourist season, the costs were so high that a considerable segment of the tourist industry decided to not even work this summer since they would lose less money this way.

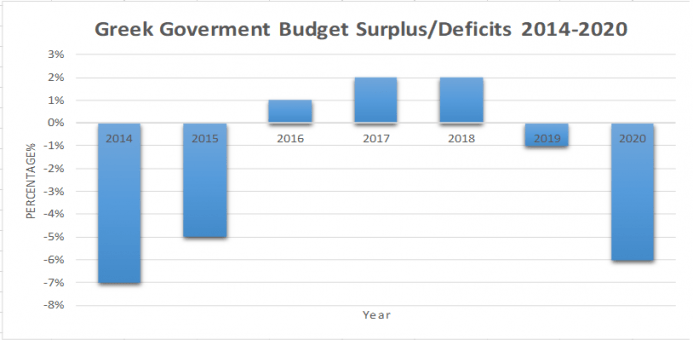

Government intervention made things even worse by failing to address the biggest problem in the economy, which is its inflexible labor laws. Rather than partially liberalizing the laws, the state made them even more restrictive and inflexible. For this reason, businessmen have failed to adjust to the corona crisis shock. Making hiring more expensive and riskier is a recipe for disaster, especially in a fragile economy that lacks savings and investments like Greece. While the spending didn’t manage to stimulate the economy, we can’t say that it had an immediate negative effect short term at least, since it was mostly financed by the European Union. On the other hand, cheap credit and loans were made possible by the ECB and by putting political pressure on banks, thus prolonging another major structural problem of the overall economy: lack of savings and more debt. The budget deficits are also a matter that needs to be addressed, since it has reached new highs, making the 2010s a lost decade for the whole economy, since the whole point of ‘’European austerity’’ was to make the debt more sustainable.

Source: Trading Economics

As the Greek minister of finance admitted the tax cuts that were made during the last few months won’t be permanent, since the new target is for Greece to have the biggest fall in debt-to-GDP in the eurozone. The state secretary of finance also talked recently about a possible new austerity program similar to that of the previous decade. On the surface, budget surpluses are a good thing and much needed, but it is important to ask these surpluses will become a reality. The tax cuts won’t be permanent, so it seems that Greeks will soon be undertaking the same failed strategy that they tried for a decade and was promoted by European officials in Brussels—high tax rates to increase government revenues but very minimal cuts in public expenditures. But the problem wasn’t the tax cuts but government spending and deficits. Deficits have a greater crowding-out effect on the private sector than just spending. At the end of the day, these deficits will have to be paid by future generations. Potential tax increases in the future would be an even bigger disaster for the private sector. The cure is worse than the disease.

The center-right government that came into power in July of 2019 has failed to liberalize the economy and make market-oriented reforms, and the pandemic has made things even worse. It hasn’t made any major tax cuts that would be permanent and could have a big impact on alleviating some of the pressure on the private sector. Deregulation was also a major issue: the Greek economy was and still is in desperate need of foreign investment; however, investment freedom hasn’t seen a significant increase, and major investments and infrastructure programs are way behind schedule. Bureaucratic obstacles extend even to the judiciary branch, making it inefficient and slow, with corruption widespread.