Part 4 – It’s different this time

Mon 12:51 pm +01:00, 29 Jun 2020This 50 year experiment in unbacked fiat money running since the USA took the world and the US Dollar off the gold standard in 1971 is coming to an end.

1. Things hidden in plain sight

2. A Fourth Turning

3. Limited Resources

4. It’s different this time

4. It’s different this time

The story of the day is that “Coronavirus causes deepest economic crisis since the Great Depression.”[1] So once the Coronavirus is conquered things will return to “normal”? Read on.

What follows is not investment advice. Think of it as pointers for your research. And, I’ll be arguing from the specific to the general, always a bad idea 🙂 We know that something strange is happening in the oil markets. We know that the world is presently in recession. We know that wealth inequality is extreme and increasing. We know also that financial ratios are signalling high levels of stress. And there’s a diversity of views on likely outcomes.

A key variable in all this is the flow of shale oil in the United States. That production increased from almost zero in 2010 to 7M bpd in 2019, and to over 9M bpd in April 2020. That was forecast to drop by over 8M bpd, blaming the drop on a lack of storage of crude oil. [2]

Toward the end of April 2020, amid competition for market share, oil prices in the futures market briefly went negative, confirming that something, somewhere, is very wrong.[3] Meanwhile US total crude oil production [20200606] is around 11.1 M bpd, after 10 week decline from a 13.1 M bpd peak. It’s reasonable to assume that the 2M bpd decline is only from shale oil production for reasons of pricing and technicals. [4]

The background to this is an exponential growth in costs of extraction, against a linear growth in demand and a linear improvement in the efficiency of extraction. [5] This has led to a division in those connected to the oil industry, with the analysis and production side warning that oil field development was increasingly risky, and that cheap oil was at an end, and the sales and investment side arguing that demand would continue to increase and that oil prices would rise because the alternatives were few and expensive. To keep the narrative simple, political and geopolitical pressures are omitted from the discussion.

Suffice to say that projections of future oil production and profits made by shale oil companies to potential investors are notoriously unreliable. In a rational world any loans to shale oil companies should have carried a very high rate of interest to compensate for the risks. That these companies were able to find adequate quantities of capital at modest rates suggests that this was not a rational world. ([6] compare with treasuries at issue dates, for example) While shale oil companies are something of an outlier, much of what follows next applies on a global scale, and to companies whose business models include much more than resource extraction. [7]

There was a time when those Ministers, Secretaries and Chancellors responsible for Government finance were happy to talk to the public about balancing budgets and would on occasion compare their task to that of a housewife balancing her budget. [8] [9] That was always more of a political message than a real view of Government finances. Those days are long gone and economic theory today centres around growing government deficits, and the management of inflation by taxation. In truth this is driven by political considerations and by the appearance of Japan to continue to function and perhaps prosper in low economic growth for decades amid increasing government debt. [10]

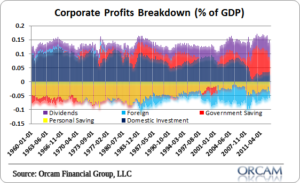

Before getting into the detail of what is going on, have a look at this chart of US Company profits, and look particularly at the years 2008-2013. The red areas are the US Government’s budget surplus or deficit. Deficit above the line, surplus below. In the years following the Great Financial Crash of 2008, US Company profits approximated to the US Government budget deficit. Think of it as toothpaste being squeezed out of a tube – it has to go somewhere, and that somewhere is the bottom line of US Companies. [11]

The technical explanation is given in Kalergi’s profit equations, and that is left to the reader to research. [12]

Think of it like this: the hand doing the squeezing is the US White House; the tube is the Federal reserve; and the toothpaste is the money created by the deficit in the US Treasury account and pushed into Companies via the big US Banks, if not directly, then by investors hungry for yield. The toothpaste has to go somewhere and eventually it ends up in the coffers of, among others, shale oil companies.

This specific instance happens because, for example, the US Government buys crude oil for storage, and pays the shale oil company for a quantity of oil that would otherwise have marginally reduced the market price of oil. The shale oil company pays its operating costs and the modest costs of finance, and the surplus is recorded as a profit. This increases the value of the company to the investors and by the wonders of leverage appears as a larger profit in some financial entity’s books.

This creates a great Moral Hazard. The present day incentives for the CEO of a public company are nominally to improve the efficiency, improve products and drive down costs to increase the company’s profitability. The above argument declares that the way to any large company in the private sector, particularly those connected to the government, is to lobby Government to increase the deficit and thus to increase private sector profits. No pain or capital needed.

Even better, if negative rates of interest are available, the greater the sums borrowed, the greater the profitability and the greater the disadvantage to companies without access to cheap borrowing rates. The result is a series Potemkin Villages in global equity stock markets, the real value of which is impossible to tell until governments deficits fall to zero and the cost of credit rises.

In the final analysis though, it seems that the price of oil is driven by geopolitics as much as anything else, including oil field technicalities, global oil storage capacity, and the sensitivity of economies to oil prices. However, low interest rates and excess quantities of credit enables the instability of the markets. As time passes and the quantities of sovereign debt increase, this tendency toward instability increases, and the greater the efforts needed by Central Banks to steady their economies and achieve albeit modest quantities of growth.

Hence this part of mineral (oil) extraction is a patch of instability within a bigger and progressively more unstable economy. Depending on the next big shock to the economy, prices could have moved into deflation or excessive inflation, or perhaps both. The government reaction globally to Covid-19 pushed economies into deflation, unemployment and recession, at a time when oil prices had fallen as result of a trade war, and at a time when global GDP appeared about ready to decline.

Note that these did not materially alter productivity, infrastructure, levels of debt or credit, or stored wealth in the form of commodities or intellectual property. Zombie companies, for the moment, continue to be the walking dead.

What happens next?

What follows is a best guess based on history. It also notes that bad outcomes can be made worse by government intervention and that the Lockdowns will end today.

Mostly, companies reopen. Some will not. Bankruptcy takes some time to work through, so, it takes some time for the bad debt to appear on bank balance sheets. Some prices rise, some fall, unemployment becomes chronic. On balance, prices fall a little and wages fall a little in the statistics, but these things are personal and local. That’s in the short term. Damage limitation by way of increased government deficit spending. [17] [18]

In the medium term, ie two or three years out, banks are allowed to go bankrupt, lending is squeezed, and tax revenues are down. Governments and banks are faced with decisions to be made about imprudent lending, for example, to shale oil companies. There follows a re-run of 1928/1929, except instead of lending to the German economy, the Banks have lent globally, and every equity market will fall.

For the gory details of how the early stages of depression evolve, read Tobias Straumann’s 1931: Debt, Crisis and the rise of Hitler, and for a somewhat different take, listen to Professor Steve Keen [9] [10]

Prices remain depressed until stored resources are exhausted, at which point prices begin to increase. Global trade, already in recession, will decline. Global markets and perhaps nation states will fragment and economies of scale are lost. All this will lead to long term declines in infrastructure and productivity. As prices begin to increase, interest rates will be increased also. When that happens, companies may be no longer able to finance their business model at affordable rates, and must adapt or die. The sovereign debt of Nation States who have offshored productive industry is at risk of default. Governments search frantically for assets, knowing that debts are so large they can never be serviced. Governments are forced beyond austerity and into nationalising companies and resources and assets at fractions of their supposed value, meanwhile markets crash or cease to operate.

Commercial real estate that cannot show a profit is worth nothing, as are resources that are no longer worth exploiting. Equity could be revalued at a few cents on the dollar, priced against precious metals.

The instability will continue until a debt reset is agreed, and as a result economic decline will proceed in a series of downward steps, each of around twenty percent of GDP, each step around seven to ten years in duration. A series of regional and civil wars will not help, leading to famines and plagues.

In 1932/1934 the US and global recovery was aided by the discovery of what was at that time the world’s biggest oil field. Even if a new and cheap form of energy was available today, for example a viable form of nuclear fusion, it may be too late to have any significant impact on the forecast declines.

So, yes, it will be different this time.

Literally today the man behind the curtain is Jay Powell, who states :

“Meanwhile, we look like we are blowing a fixed-income duration bubble right across the credit spectrum that will result in big losses when rates come up down the road. You can almost say that that is our strategy.” [13] [14]

The received wisdom is that the Fed “can’t make unprofitable businesses profitable” but as demonstrated above, given enough government deficit, that is exactly what has been happening. This 50 year experiment in unbacked fiat money running since the USA took the world and the US Dollar off the gold standard in 1971 is coming to an end. [15]

To be truly different however, this premise has to end : “Let me issue and control a nation’s credit and I care not who writes its laws.” — Mayer Amschel Rothschild (1744-1812). For that to happen, debt and credit have to become worthless, and the linkage between credit issuance and GDP growth has to end. The USA is almost there. [16] [1] https://www.rt.com/business/485313-wto-covid19-deepest-economic-crisis/

[2] https://thedeepdive.ca/us-shale-oil-production-reduced-by-record-drop-amid-global-oversupply/ [3] https://eu.usatoday.com/story/money/2020/04/21/oil-prices-turn-negative-what-does-mean/2994929001/ [4] https://www.zerohedge.com/energy/us-oil-dominance-coming-end [5] https://www.youtube.com/watch?v=dLCsMRr7hAg – CGEP: Global Oil Market Forecasting: Main Approaches & Key Drivers with Steven Kopits [6] https://markets.businessinsider.com/bonds/6_625-chesapeake-energy-bond-2020-us165167cf27 [7] https://www.youtube.com/watch?v=TFyTSiCXWEE – Peak mining & implications for natural resource management – Simon Michaux [8] https://www.margaretthatcher.org/document/107248 [9] https://www.youtube.com/watch?v=KIaXVntqlUE – Meet the Renegades Steve Keen [10] https://renegadeinc.com/cost-getting-wrong/ [11] http://www.pragcap.com/why-hasnt-the-budget-deficit-decline-hurt-corporate-profits-more/ [12] https://wiiw.ac.at/kalecki-s-profit-equation-after-80-years-dlp-3020.pdf [13] https://www.zerohedge.com/markets/total-us-debt-increases-1-trillion-one-month“What is stunning, however, is the recent pace of increase: total debt was “only” $23.5 trillion on March 23, the day the Fed unleashed unlimited QE, meaning that in two and a half months, the US has added $2.5 trillion in debt. And the punchline: the US added the last trillion dollars in the shortest time on record, achieving this remarkable feat in just one month, since May 4, when total debt was just under $25 trillion.”

[14] https://www.zerohedge.com/markets/700-billion-gorilla-roomThe Treasury has to flood the US with $700 Billion before the end of June.

“While some have speculated that it will very difficult for the Treasury to allocate all those funds over the next two weeks, especially since there is virtually no demand for the remaining $140BN in unused PPP funds, on Thursday Steven Mnuchin sought to ease concerns, saying that more money is about to flow out of the government’s coffers. Of the roughly $3 trillion of pandemic relief, about $1.6 trillion has been used, and “we’re busy working on disbursing the rest of the money,” he told reporters in a video conference. “There’s a lot of money that hasn’t been allocated” yet, and over the next month $1 trillion will be pumped into the economy, he said. It was, however, not clear just how this money would be “pumped into the economy.” The problem, as Bloomberg notes, is that while investors have been able to absorb the record barrage of new debt, which has seen US Federal Debt increase by $1 trillion in the past month, rising above $26 trillion for the first time ever this week…”

[15] https://mises.org/wire/hidden-link-between-fiat-money-and-increasing-appeal-socialism [16] https://www.zerohedge.com/markets/biggest-credit-impulse-history-prompting-some-very-awkward-questions [17] https://www.zerohedge.com/geopolitical/covid-shock-dollar“The US Congress has moved with uncharacteristic speed to provide relief amid a record-setting economic free-fall. The Congressional Budget Office expects unprecedented federal budget deficits averaging 14% of GDP over 2020-21. And, notwithstanding contentious political debate, additional fiscal measures are quite likely. As a result, the net domestic saving rate should be pushed deep into negative territory. This has happened only once before: during and immediately after the 2008-09 global financial crisis, when net national saving averaged -1.8% of national income from the second quarter of 2008 to the second quarter of 2010, while federal budget deficits averaged 10% of GDP.”

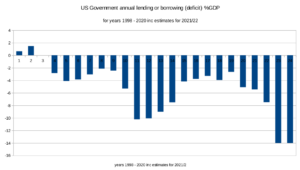

[18] Image source data : US Bureau of Economic Analysis, Tax Receipts, Table 3.2 “Net lending or net borrowing” and [17]